CPO Outlook Q2/2025

Explore dropping procurement sentiment as cost control takes precedence over innovation amid rising market pressures and ongoing compliance challenges.

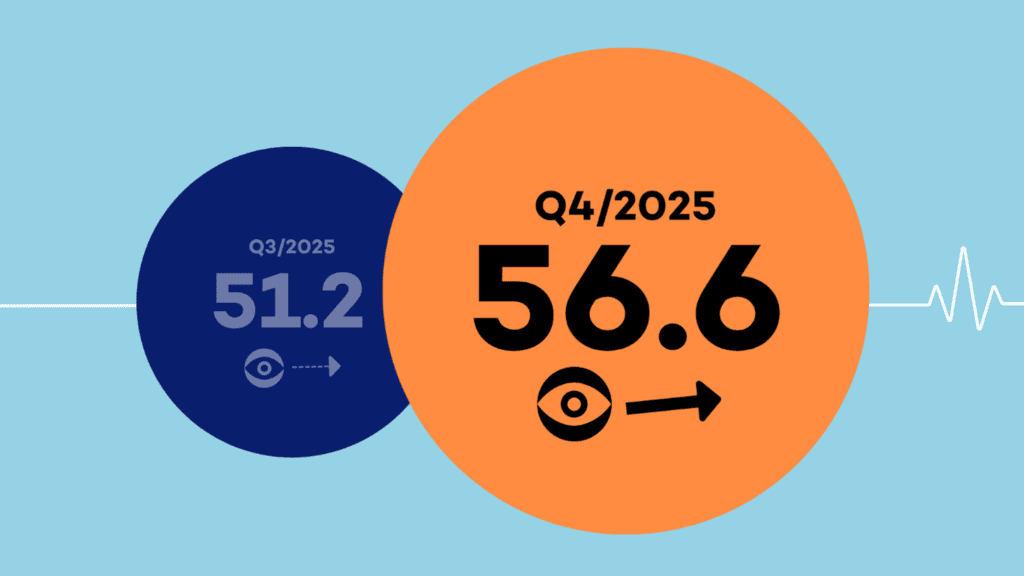

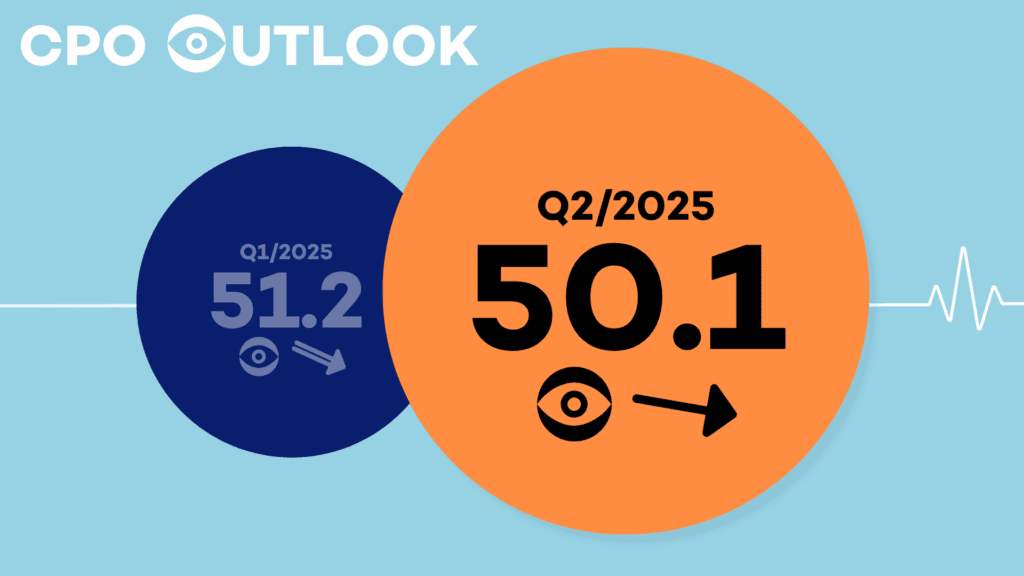

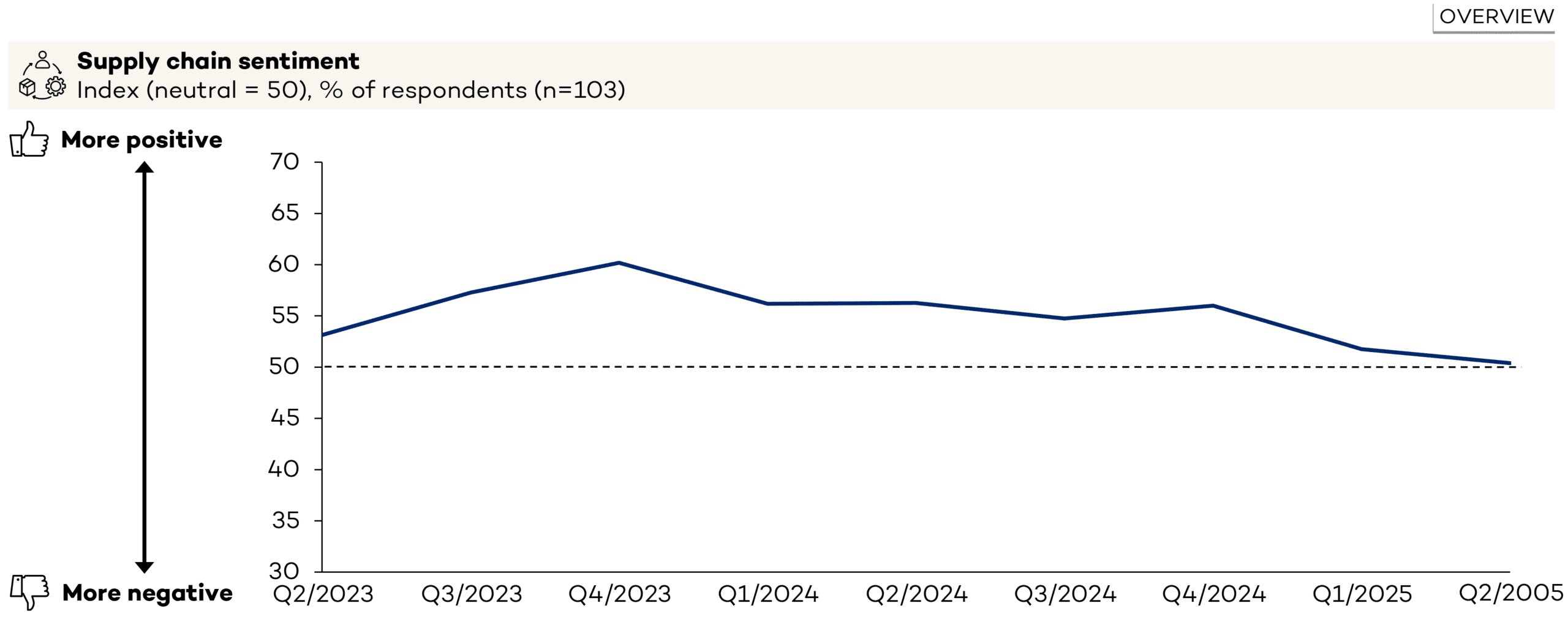

The Outlook: Eurozone Supply Chain Sentiment Drops to Lowest Level Since 2022 Amid Growing Market Volatility

What’s driving this change?

- Ongoing tariff uncertainty, with uneven preparation for U.S. policy shifts

- Rising cost pressure, forcing companies to double down on short-term savings

- Geopolitical instability, from global conflicts to regulatory disruption

- Inconsistent risk management, with many firms reacting ad hoc

- Strategic reprioritisation, as cost and quality take precedence over sustainability

- Reduced planning reliability, making long-term transformation harder to justify

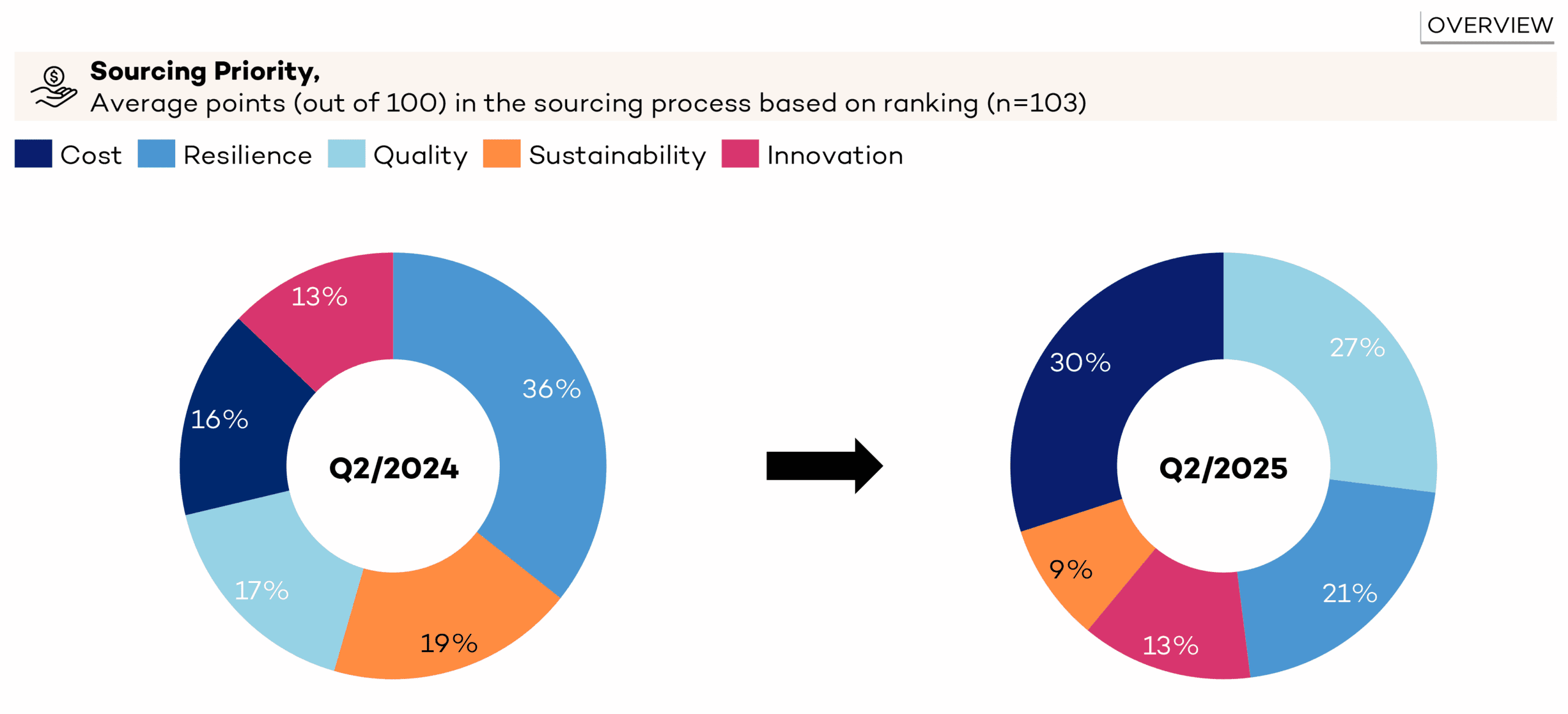

Quality (27%) and Cost (30%) First: Reliability and Excellence Regain Top Priority Amidst Shifting Sustainability Focus

Short-term focus (based on immediate impacts and actions)

- Cost-out initiatives, to protect margins under inflation and regulatory strain

- Supplier diversification, to reduce exposure to geopolitical and tariff risks

- Nearshoring and reshoring, to boost supply stability amid global uncertainty

-

Contract adjustments, reacting to shifting legal and compliance environments

Mid-term focus (based on strategic responses and planning)

- Procurement analytics and forecasting, to improve resilience and scenario planning

- Long-term supplier partnerships, aiming to stabilise supply chains under pressure

- Organisational change, including realignment of procurement processes

- Compliance readiness, with more focus on regulatory adaptation and ESG tracking

Looking Forward

Procurement leaders are shifting from transformation to tactical execution. As uncertainty around tariffs, costs, and compliance grows, organisations are prioritising control over change.

The focus will stay on cost reduction, risk mitigation, and strengthening supplier relationships. While digital tools and analytics are gaining relevance, long-term innovation and sustainability efforts may continue to take a back seat. Expect a pragmatic, resilience-first approach — with flexibility and speed valued over strategic overhaul.