Rare Earths. High Stakes. No Time to Wait.

China controls over 90% of global rare earth processing — and the pressure is mounting. Export bans, supply shocks, and rising costs are shaking entire industries. From EV makers to defense contractors, those who act now will lead. We help you build resilient supply chains, secure strategic access, and stay ahead in a fractured global market.

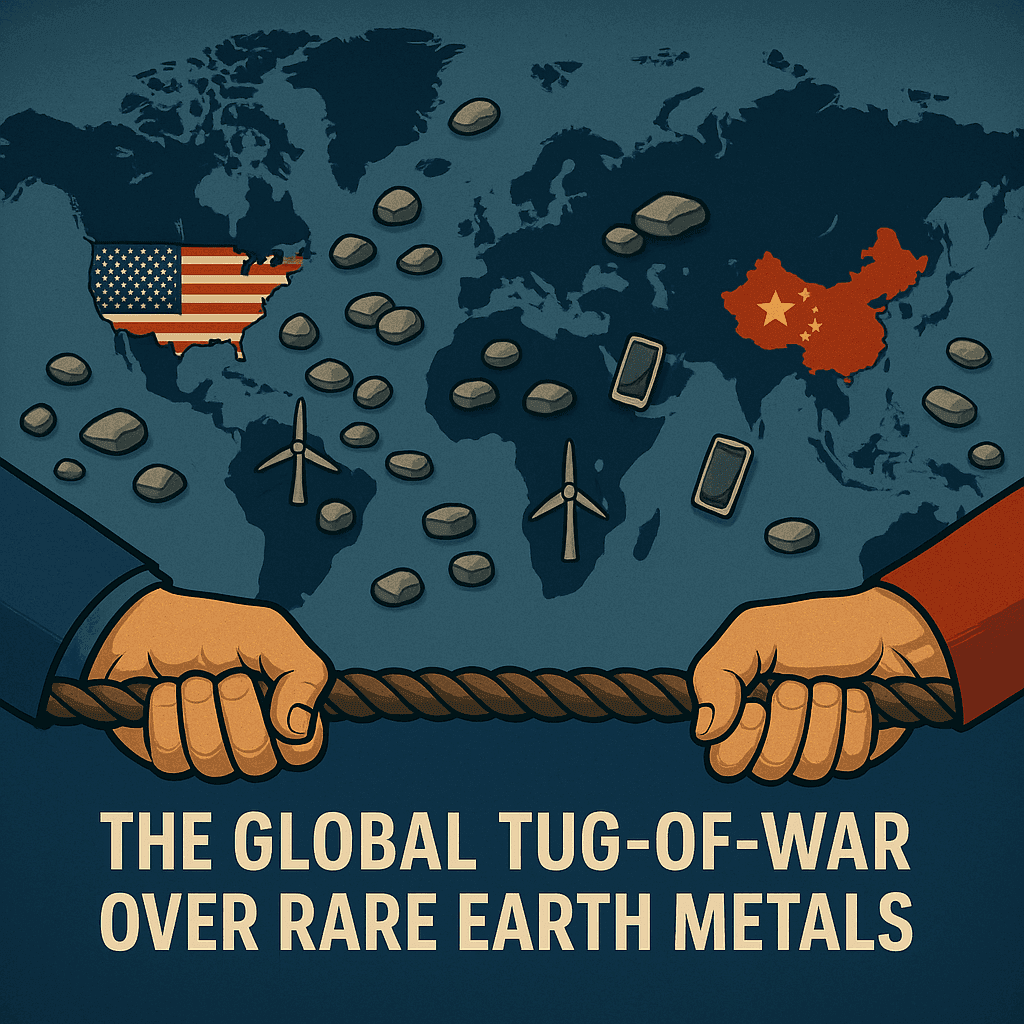

The Global Tug-of-War Over Rare Earth Metals

In the high-stakes game of global trade and power, rare earth metals have quietly become one of the most critical, and contested, resources on the planet. With China controlling over 90% of the world’s processing capacity, supply chain disruptions and export controls are sending shockwaves across industries. From electric vehicle manufacturers and wind turbine producers to defence contractors and tech companies that rely on high-performance magnets, the pressure is on.

As geopolitical tensions rise, with the U.S. striking rare earth deals from Greenland to Ukraine, the race for secure access is reshaping trade policy, corporate strategy, and the future of innovation.

What Are Rare Earth Metals and Why Do They Matter?

Rare earth metals are a group of 17 chemically similar elements that are essential to the performance of a wide range of modern technologies. Despite their name, they're not actually rare in the earth’s crust, but they’re difficult and costly to extract and process. These metals are critical in producing high-strength permanent magnets, which are used in everything from electric vehicle motors and wind turbines to smartphones, medical devices, and military equipment like guided missiles and radar systems. Without a steady supply, key sectors of the global economy risk grinding to a halt.

Why is there a Global Crisis?

The rare earth metals crisis stems from a critical imbalance: while many countries depend on these metals, China controls the lion’s share of both mining and, more crucially, processing. This dominance has evolved over decades, turning what was once a strategic advantage into a global vulnerability.

Since the 1990s, China has ramped up its control over mining and processing, eventually cornering the market. Despite global pushback, including a 2014 World Trade Organisation ruling, China still controls 85% of processing and over 90% of rare earth magnet production. The geopolitical tensions between the U.S. and China have further exacerbated the situation. In April 2025, China imposed export curbs on seven types of rare earths and related magnets. These actions are seen as part of China's strategic response to escalating trade disputes, including U.S. restrictions on China's semiconductor industry.

This confluence of factors has transformed the rare earth metals sector into a flashpoint for global supply chain stability. Amid growing instability in U.S.-China relations, manufacturers around the world are under increasing pressure to diversify their supply chains and reduce dependency

The Impact…

- Overdependence on China: …obviously

- Lack of Domestic Processing: The U.S. mines rare earths but lacks refining capacity, forcing it to rely on Chinese processors. This bottleneck hikes costs and slows production.

- Slow Development of Alternatives: Building new mines and refineries takes years, and with regulatory hurdles and local pushback, rapid diversification is off the table.

- Rising Costs and Volatility: Supply uncertainty is driving up rare earth prices, hitting EV makers, renewable energy firms, and electronics hardest.

Environmental and Ethical Issues: Rare earth mining is environmentally damaging and often rife with labour issues. Companies are under pressure to source responsibly, but it’s complicated and costly.

Who’s Feeling the Heat?

As rare earth metal supply disruptions grow increasingly unstable, entire industries are starting to feel the strain. EV makers are scrambling for magnets, wind and solar projects are facing costly delays, and consumer tech brands are slowing rollouts as component prices surge. Ford has already been forced to act, suspending production for a week at its Chicago assembly plant, where the Explorer is manufactured. And that's likely just the beginning. Defence and aerospace contractors are eyeing supply risks with growing unease, while industrial magnet manufacturers and high-tech economies like the U.S., Germany, Japan, and South Korea are watching competitiveness slip through their fingers. If current trends continue, this could mark the early stages of a much broader industrial reckoning.

How To Stay Ahead in the Race for Rare Earths

If your rare earth strategy involves sipping coffee and doomscrolling headlines about Trump vs. China each morning, you're already behind. The clock’s ticking and the smart players are already moving.

In the short term, nimble manufacturers are diversifying fast, tapping into alternative suppliers across Europe, the U.S., and Oceania, regions beyond the reach of Chinese export controls. Accelerated tendering processes are opening doors to critical materials, while leaner, smarter stockpile optimisation strategies make sure every gram is pulling its weight.

But true resilience isn’t a quick fix. It’s a long game. That means forging direct ties with miners in politically stable regions, investing in next-gen substitution technologies, and planting flags in tomorrow’s mining hotspots. Lock in buffer stock agreements to keep components on hand, no matter what geopolitical tensions arise and secure your supply to ensure business continuity.

At H&Z, we know this market inside and out. We’ve helped multiple clients navigate supply chain disruptions, diversify sourcing strategies, and connect with a vast network of suppliers to build more resilient operations.

Get in Contact with our Experts:

Oliver Jones

You might be also interested in:

Your search result is empty. Try another filter combination.